(Be sure to ask us to find the “Actual” value of your vehicle. The value is often very different to what you think.)

Option 1: you may be able to speak with your Bankruptcy Trustee (the person who looks after you during your bankruptcy) and ask them if you can pay off the difference over the term of your bankruptcy. Here’s an example. Let’s say that your vehicle is worth $15000 and you would like to keep it. You could speak with the trustee and let them know that you realise you can only keep a car up to the value of $8000 but that you would like to keep the car and pay off the difference over the next year or two. Often you will find the Trustee very helpful and accommodating and will be more than happy to work with you on this.(We are happy to negotiate this for you)

Option 2: You could simply hand the vehicle to your trustee. He can then arrange for it to be sold and once it is sold your trustee will give you back $8000 from the sale of the vehicle and pay the rest of the money to your creditors. (People you owed money to.) You can then use this $8000 to go and buy another vehicle.

If your vehicle is under secured finance the situation is quite different. Here are the usual scenarios that exist regarding financed vehicles and Bankruptcy.

Scenario 1: Often you will find that you owe more on the vehicle than what it is worth. If this is the case and your finance company agree to let you keep the loan, then you can keep the vehicle so long as you continue to pay the loan. (That’s right, you can choose to keep a loan even if you go bankrupt!)

Scenario 2: If your vehicle is worth up to $8000 more than you have left on your loan and your finance company agree to let you keep the loan, then you can keep it. For example, if you have a vehicle worth $20,000 and your loan is only $12,000 you can keep the vehicle as you only own $8000 worth of the equity in the vehicle. If you are unsure, ask us.

Scenario 3: If the vehicle is worth $8000 or more than the loan, then you will again need to work something out with your Trustee to pay off the difference. (We can negotiate this for you if you want us to.)

Often your house is your castle and to lose it in Bankruptcy can feel like a real blow. There may be ways that you can keep your house but that decision all comes down to your understanding of Bankruptcy and the options available to you, so be sure to involve us in this process.

Firstly you need to work out how much “Equity” there is in your property.

Equity is the difference between how much the property is worth and how much you owe on it. For example, if your property is worth $500,000.00 and you owe $200,000.00 on your mortgage, then there is $300,000.00 worth of equity. This is how much of the property you own.

Whether you own a property yourself or it is owned by 2 or more people doesn’t change the options available to you, but it does change the way you work out how much equity you own in the property. For example if your house was owned equally by two people instead of just you, then each person owns half the equity in the property, meaning your portion would be $150,000.00 instead of $300,000.00.

Once you have worked out how much equity there is in the property and how much of this you personally own, then some decisions can be made. Here are the options:

Option 1: If you have NO EQUITY in your property then the trustee may not be interested in trying to sell it. In this situation, you can work with your bank and if they agree, you may be able to negotiate keeping your mortgage, and your home. In most cases your Bank usually agrees to this unless you are very behind in mortgage payments.

Option 2: If you have a LITTLE BIT OF EQUITY in your home, usually anywhere between $10k and $50k, then you may be able to work with the trustee to keep your home and pay off any equity you have to them over the next few years. This money is then used to pay off your creditors. Organising this can be quite complicated, but we can take care of this for you.

Option 3: If you have A LOT OF EQUITY then the whole process can become a little tricky but there are still options available to you. To find out what you can do and how to do it, be sure to contact us and give us the full details of your property. We will then work through your options and help you find a solution.

This is a very common question because for some reason people believe that they are banned from overseas travel when they go bankrupt. This is not the case.

If you choose to travel overseas you need to complete a form and send it to your Trustee for permission to go, but this is usually just a formality and in almost every case you will be permitted to travel.

There are a few circumstances where the trustee may not agree to your going overseas. These include:

Permission is at the discretion of the trustee.

So yes, you can travel overseas and you can travel as often as you like, you simply need to get permission from your trustee. If you do wish to travel we can assist you in obtaining permission and completing the application to leave Australia.

You can go bankrupt 2 ways.

Forced Bankruptcy: You can be forced into Bankruptcy by one of your creditors. They do this by applying to the courts for a judgement against you and once this is done, if you do not pay, you will be made bankrupt. Forced Bankruptcy is usually a VERY stressful process. You may be required to attend court, involve lawyers, complete documents, provide detailed personal financial reports and much more. If someone has already started this type of action against you, contact us and we can attend to it for you.

Voluntary Bankruptcy: This is where you choose to take control and go bankrupt yourself.

Although the process of Forced Bankruptcy can be very traumatic, the process of Voluntarily Bankruptcy can also be quite complicated and stressful. BUT DON’T PANIC, we assist and guide you through the whole process

With Voluntary Bankruptcy, the answer is NO!

You won’t be dragged off to court, you won’t be charged as a criminal, you won’t have your name splashed all over the media and up in lights. The process of Voluntary Bankruptcy is a very personal process.

Your bankruptcy will be recorded on your personal Credit file for 5 years, but all things going smoothly, your actual bankruptcy only goes for a period of 3 years and one day. After that time you will be able to go out and apply for a loan or whatever you need. This is called your discharge date, or the date your Bankruptcy is discharged.

Once your Bankruptcy is discharged, it is over. You will simply receive a letter informing you that your bankruptcy has now been discharged.

It is as though you have just been financially born again. A wonderful feeling.

With Voluntary Bankruptcy, the answer is NO!

You won’t be dragged off to court, you won’t be charged as a criminal, you won’t have your name splashed all over the media and up in lights. The process of Voluntary Bankruptcy is a very personal process.

Your bankruptcy will be recorded on your personal Credit file for 5 years, but all things going smoothly, your actual bankruptcy only goes for a period of 3 years and one day. After that time you will be able to go out and apply for a loan or whatever you need. This is called your discharge date, or the date your Bankruptcy is discharged.

Once your Bankruptcy is discharged, it is over. You will simply receive a letter informing you that your bankruptcy has now been discharged.

It is as though you have just been financially born again. A wonderful feeling.

The usual term of Bankruptcy is 3 years and 1 day.

Yes. There is a process called a “Composition” where, during the period of your bankruptcy, you are able to make an offer to your creditors. If they accept your offer as full and final settlement of your accounts, then your bankruptcy will be annulled.

If you are currently bankrupt or are considering bankruptcy, this is something you may wish to consider if you feel that bankruptcy may have a detrimental effect upon any future decisions.

Yes. There is a process called a “Composition” where, during the period of your bankruptcy, you are able to make an offer to your creditors. If they accept your offer as full and final settlement of your accounts, then your bankruptcy will be annulled.

If you are currently bankrupt or are considering bankruptcy, this is something you may wish to consider if you feel that bankruptcy may have a detrimental effect upon any future decisions.

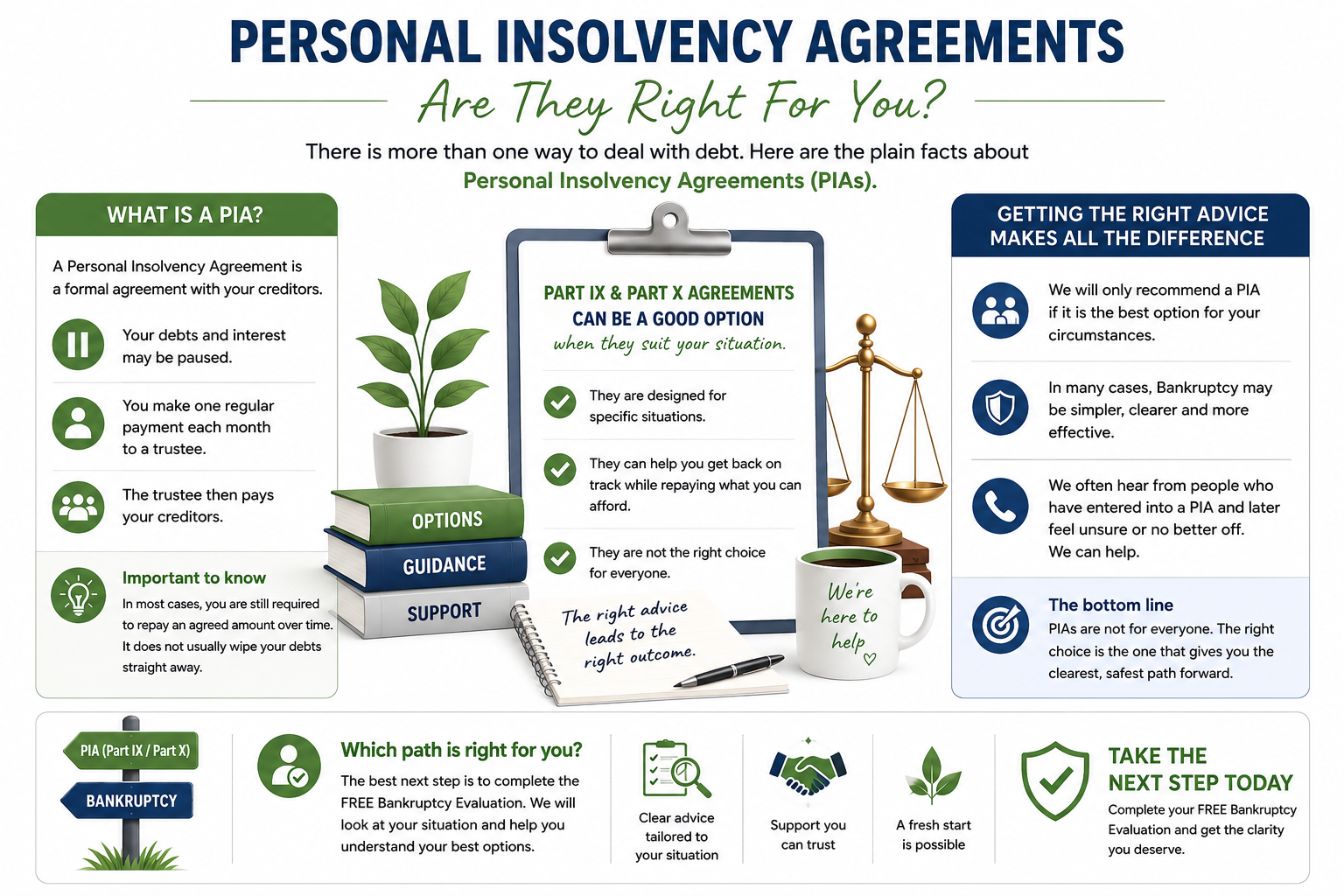

There are a number of Personal Insolvency agreements that are available to you.

There are a number of Personal Insolvency agreements that are available to you.

Debt agreements such as a Part 9 or Part 10 may be an option for individuals struggling with crippling debt. However, it is important to seek advice on your situation as in some cases organisations may recommend Debt Agreements for reasons other than it being the best solution for their client. If you are currently in a debt agreement and are struggling to make the repayments, then it is important to seek further advice. If you cannot continue to service your debt agreement then you can simply stop paying it and arrange to be released from it and you can then choose to go bankrupt instead. If you have found yourself in this situation, simply complete our Bankruptcy Eligibility Checklist and we can help you out of your debt agreement and into a Fresh Start through Bankruptcy.

Debt agreements such as a Part 9 or Part 10 may be an option for individuals struggling with crippling debt. However, it is important to seek advice on your situation as in some cases organisations may recommend Debt Agreements for reasons other than it being the best solution for their client. If you are currently in a debt agreement and are struggling to make the repayments, then it is important to seek further advice. If you cannot continue to service your debt agreement then you can simply stop paying it and arrange to be released from it and you can then choose to go bankrupt instead. If you have found yourself in this situation, simply complete our Bankruptcy Eligibility Checklist and we can help you out of your debt agreement and into a Fresh Start through Bankruptcy.

A TDP is an option you may wish to consider whilst deciding if you wish to go Bankrupt.

A TDP is a “Temporary Debt Protection”. The Federal Government allow those who apply for a TDP, a series of protections for an extended period of time. This time allows you to research your options and decide what to do.

What does a TDP do?

A Temporary Debt Protection (TDP) allows you the following protections:

A TDP is an option you may wish to consider whilst deciding if you wish to go Bankrupt.

A TDP is a “Temporary Debt Protection”. The Federal Government allow those who apply for a TDP, a series of protections for an extended period of time. This time allows you to research your options and decide what to do.

What does a TDP do?

A Temporary Debt Protection (TDP) allows you the following protections:

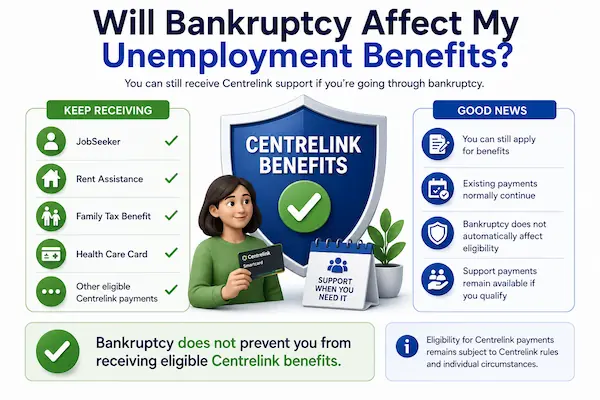

The short answer to this is NO. You are still able to apply for and receive unemployment benefits through Centrelink as a bankrupt. If you are already receiving these benefits they will continue as they currently are and if you are yet to apply for Unemployment benefits, you simply apply a usual. You are also able to continue to receive other benefits such as Family Allowance, rent assistance, a health care card and most other government benefits if you qualify.

The short answer to this is NO. You are still able to apply for and receive unemployment benefits through Centrelink as a bankrupt. If you are already receiving these benefits they will continue as they currently are and if you are yet to apply for Unemployment benefits, you simply apply a usual. You are also able to continue to receive other benefits such as Family Allowance, rent assistance, a health care card and most other government benefits if you qualify.

Your Centrelink debt will be taken care of as part of your Bankruptcy. However, if it is has been found that your Centrelink debt was fraudulent and the courts have found you guilty and charged you with fraud or dishonesty, then this Centrelink debt will not be covered as part of bankruptcy and you will be required to pay it back. For more clarification on this please contact us.

Your Centrelink debt will be taken care of as part of your Bankruptcy. However, if it is has been found that your Centrelink debt was fraudulent and the courts have found you guilty and charged you with fraud or dishonesty, then this Centrelink debt will not be covered as part of bankruptcy and you will be required to pay it back. For more clarification on this please contact us.

|

Bankruptcy does NOT stop you from working and normally your employer does not need to know, nor will they be told that you are bankrupt. However, there are some restrictions to be aware of:

|

Yes, however there may be circumstances where Landlords ask you to let them know if you are, or if you have become bankrupt. Each situation is different so please read through your rental agreement and find out what the requirements are.

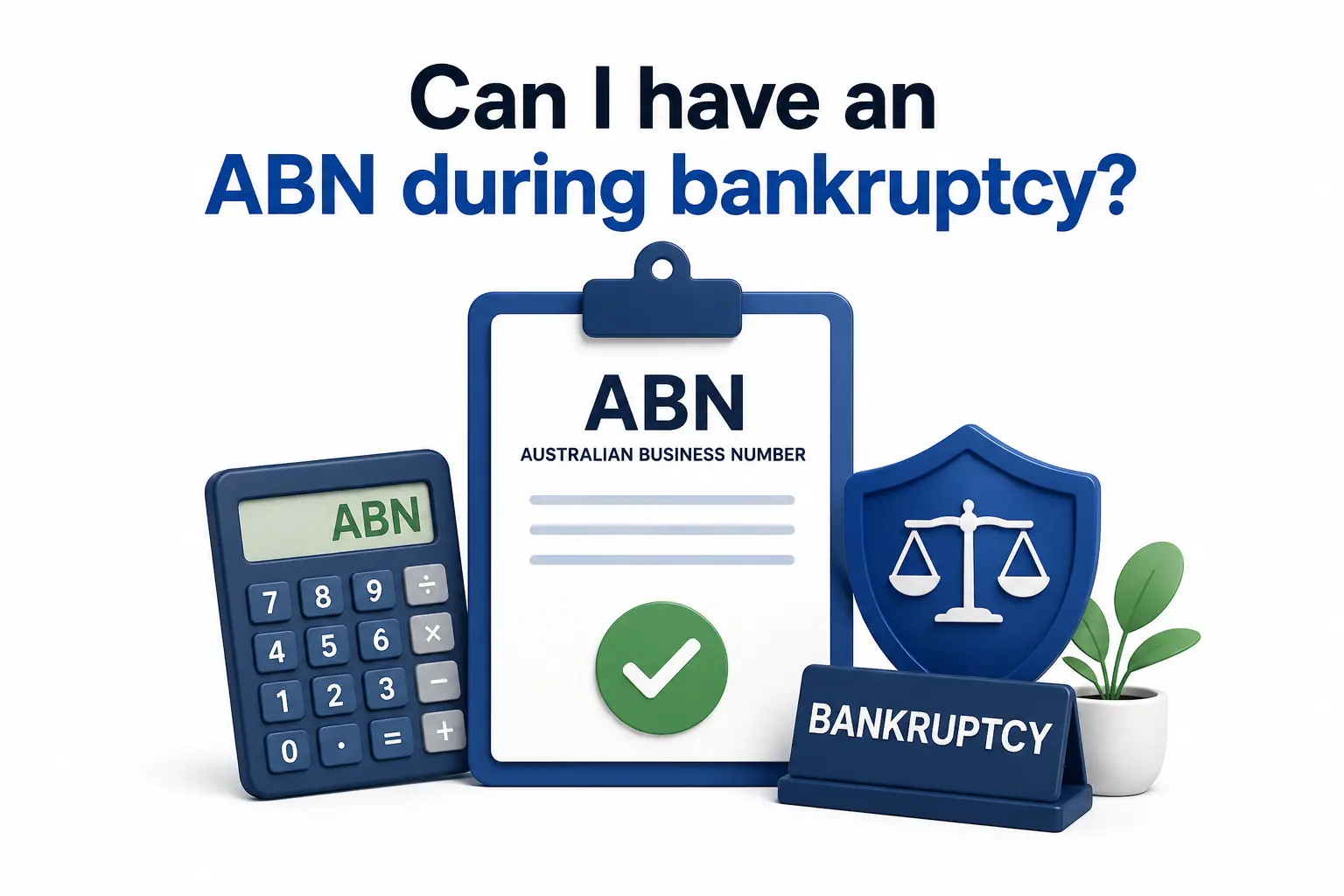

While you are Bankrupt you are able to register an ABN (or keep your existing ABN if you are already a sole trader) and run a business as a sole trader (there are some requirements and restrictions to this, so call us to find out the details). However, you are not able to be the Director of a Company while you are bankrupt, unless you are given approval by the courts.

So, in short, YES you can run a business as a bankrupt. It is not the Government’s intention to “kill off your ambitions and put you into hibernation” for 3 years, they simply need to be sure that you meet your obligations as a bankrupt.

While you are Bankrupt you are able to register an ABN (or keep your existing ABN if you are already a sole trader) and run a business as a sole trader (there are some requirements and restrictions to this, so call us to find out the details). However, you are not able to be the Director of a Company while you are bankrupt, unless you are given approval by the courts.

So, in short, YES you can run a business as a bankrupt. It is not the Government’s intention to “kill off your ambitions and put you into hibernation” for 3 years, they simply need to be sure that you meet your obligations as a bankrupt.

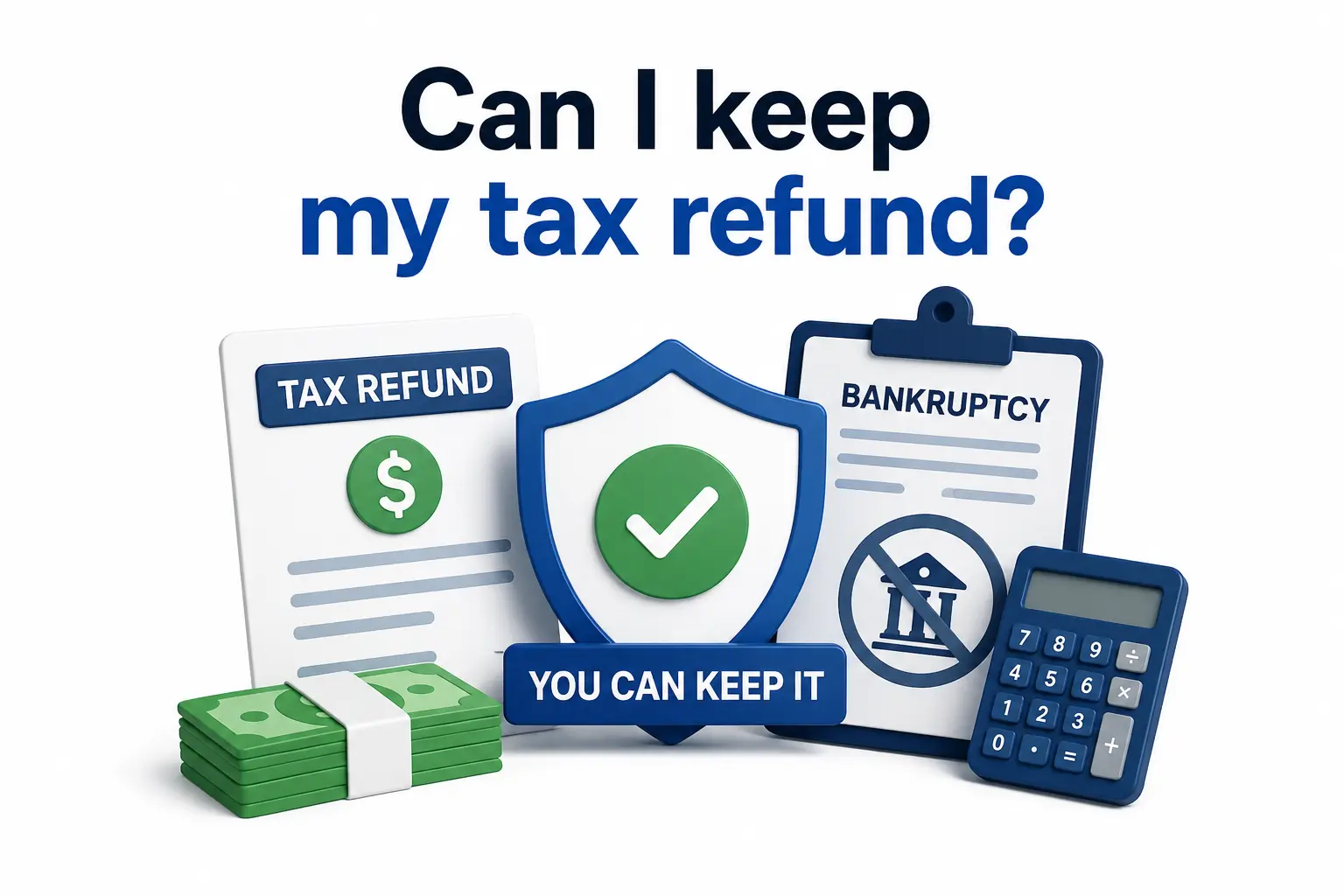

If you owed money to the tax office at the time of your bankruptcy, any refund you are entitled to during the period of bankruptcy may be retained by the tax office to offset the amount owing. Tax refunds owing to you prior to the date of your bankruptcy can be claimed by the trustee. Tax refunds owing to you during your bankruptcy will be treated as income for income assessment purposes. After discharge, any debt still outstanding to the tax office which formed part of the bankruptcy cannot be recovered by the tax office. Tax refunds after discharge are paid to you. Regardless of bankruptcy you are still responsible for lodging your Income Tax Returns.

If you owed money to the tax office at the time of your bankruptcy, any refund you are entitled to during the period of bankruptcy may be retained by the tax office to offset the amount owing. Tax refunds owing to you prior to the date of your bankruptcy can be claimed by the trustee. Tax refunds owing to you during your bankruptcy will be treated as income for income assessment purposes. After discharge, any debt still outstanding to the tax office which formed part of the bankruptcy cannot be recovered by the tax office. Tax refunds after discharge are paid to you. Regardless of bankruptcy you are still responsible for lodging your Income Tax Returns.

If you enter bankruptcy, you will find that most debts are covered. This means that you no longer have to repay them.

In some cases, your trustee may sell your assets or use compulsory payments to help pay your debts.

Your debts are all discharged, meaning they are written off by your creditor (the person or organization you owe them to). Of course if you have a secured debt, which is a debt that is secured against an asset, such as a Housing loan and you decide that you would like to keep the debt through your bankruptcy, then the Bank will maintain title over the asset and you won’t be discharged from that debt but will maintain it and as long as you keep paying it off you can maintain the asset.

All other debts will be written off except for a few such as fines for breaches of the law (eg: speeding fines), debts arising from fraud, maintenance payments and Child Support, some debts due to Centrelink and accumulated HECS (Higher Education Contribution Scheme).

If you enter bankruptcy, you will find that most debts are covered. This means that you no longer have to repay them.

In some cases, your trustee may sell your assets or use compulsory payments to help pay your debts.

Your debts are all discharged, meaning they are written off by your creditor (the person or organization you owe them to). Of course if you have a secured debt, which is a debt that is secured against an asset, such as a Housing loan and you decide that you would like to keep the debt through your bankruptcy, then the Bank will maintain title over the asset and you won’t be discharged from that debt but will maintain it and as long as you keep paying it off you can maintain the asset.

All other debts will be written off except for a few such as fines for breaches of the law (eg: speeding fines), debts arising from fraud, maintenance payments and Child Support, some debts due to Centrelink and accumulated HECS (Higher Education Contribution Scheme).

The cost of obtaining assistance through My Bankruptcy, for your bankruptcy application will vary according to your circumstances and the complexity of your case.

There are special Bankruptcy Assistance rates for the following:

The cost of obtaining assistance through My Bankruptcy, for your bankruptcy application will vary according to your circumstances and the complexity of your case.

There are special Bankruptcy Assistance rates for the following:

That depends on what they are. If you own a house, a car, a boat, a jet ski, a motor bike or anything MAJOR in value you need to call us so that we can work out the best option for you.

In most cases you are able to keep your personal motor vehicle. This of course depends on the value of the vehicle but very seldom are cars lost through the process of Bankruptcy.

As for your household furniture, you will keep this. Bankruptcy is not as it used to be. In the past you would lose everything you owned of value. Today, you keep your household furniture and personal items. Yes, that includes your Big Screen TV and stereo!

If you are a Trades person or have tools of trade, in most cases you will also be able to keep most or all of these up to a specified value. Simply call us to find out more.

While there are certainly consequences to Bankruptcy, many potential Bankrupts have heard horror stories and rumours of others who were kicked out of their rental home or booted out on to the street in a matter of days from the home they were buying, while someone came in and rifled through their personal household belongings. This doesn’t happen. Bankruptcy is an opportunity to start again, not a death sentence!

That depends on what they are. If you own a house, a car, a boat, a jet ski, a motor bike or anything MAJOR in value you need to call us so that we can work out the best option for you.

In most cases you are able to keep your personal motor vehicle. This of course depends on the value of the vehicle but very seldom are cars lost through the process of Bankruptcy.

As for your household furniture, you will keep this. Bankruptcy is not as it used to be. In the past you would lose everything you owned of value. Today, you keep your household furniture and personal items. Yes, that includes your Big Screen TV and stereo!

If you are a Trades person or have tools of trade, in most cases you will also be able to keep most or all of these up to a specified value. Simply call us to find out more.

While there are certainly consequences to Bankruptcy, many potential Bankrupts have heard horror stories and rumours of others who were kicked out of their rental home or booted out on to the street in a matter of days from the home they were buying, while someone came in and rifled through their personal household belongings. This doesn’t happen. Bankruptcy is an opportunity to start again, not a death sentence!

As a Bankrupt, you can earn as much as you want as a bankrupt.

However, there are some earning “thresh holds” that apply to you for the term of your bankruptcy that you need to be aware of. Once you reach these thresh holds you will need to pay the Trustee (The trustee is the Individual or organization that is administrating your bankruptcy) 50% of everything you earn above this amount. This money is then paid back to your creditors (The people you owe money to).

Here is the current thresh hold limit:

As a Bankrupt, you can earn as much as you want as a bankrupt.

However, there are some earning “thresh holds” that apply to you for the term of your bankruptcy that you need to be aware of. Once you reach these thresh holds you will need to pay the Trustee (The trustee is the Individual or organization that is administrating your bankruptcy) 50% of everything you earn above this amount. This money is then paid back to your creditors (The people you owe money to).

Here is the current thresh hold limit: